The Net Worth Reality: Why Income Alone Does Not Make You Wealthy

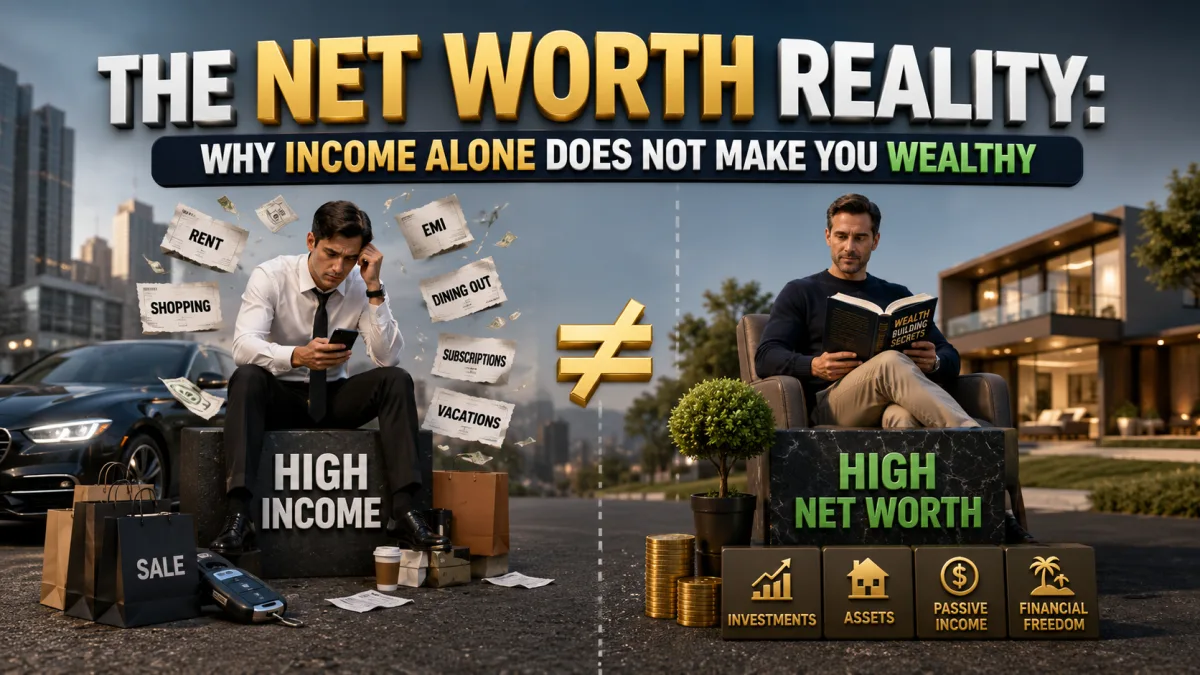

High income does not always mean wealth.

This is one of the most important financial truths a person can learn, and it is also one of the most commonly ignored. Society often treats income as the main sign of success. People ask what someone earns, what job title they hold, what business they run, what neighborhood they live in, what car they drive, or what lifestyle they appear to afford.

But income is only part of the story.

A person can earn a large salary and still be financially fragile. They can live in an expensive home, drive a luxury vehicle, travel often, wear expensive clothes, and still have very little actual wealth. Their life may look successful from the outside while being supported by debt, high monthly obligations, and constant pressure to keep earning more.

Another person may earn less, live more quietly, invest consistently, reduce debt, own appreciating assets, and build a stronger financial foundation over time. Their lifestyle may look ordinary, but their balance sheet may be improving every year.

The difference is net worth.

Income measures money coming in. Net worth measures what remains, what grows, and what is truly yours after subtracting what you owe. Income creates opportunity. Net worth reveals whether that opportunity is being converted into wealth.

This distinction changes the way you think about money. It moves the focus from appearance to ownership, from salary to assets, from spending power to financial strength. It also exposes why many high earners feel stressed, why some modest earners become financially secure, and why wealth often grows quietly long before it becomes visible.

What Is Net Worth?

Net worth is the difference between what you own and what you owe.

The formula is simple:

Net Worth = Assets − Liabilities

Assets are things you own that have financial value. They may include cash, savings, investments, retirement accounts, real estate equity, business ownership, valuable property, and other resources that can strengthen your financial position.

Liabilities are what you owe. They may include credit card balances, student loans, car loans, personal loans, mortgages, unpaid taxes, business debt, and other obligations that reduce your financial position.

If your assets are worth $300,000 and your debts total $100,000, your net worth is $200,000.

That number gives a clearer picture of financial health than income alone. Someone earning $300,000 per year but owing more than they own may have a weaker financial position than someone earning $80,000 per year with growing investments, low debt, and steady savings.

Net worth is not about judging a person’s value. Human worth and financial net worth are completely different things. Net worth is simply a financial measurement. It shows whether your financial position is strengthening or weakening over time.

That measurement matters because money can be deceptive when viewed only through monthly income. A paycheck can create the feeling of progress even when wealth is not growing. Net worth cuts through that illusion.

Why Income Can Be Misleading

Income is visible. Wealth is often invisible.

Income can buy impressive things quickly. Wealth usually builds quietly through ownership, patience, and discipline. This is why people often confuse a high-earning lifestyle with financial success. They see the purchases, but not the debts. They see the home, but not the mortgage pressure. They see the car, but not the payment. They see the travel, but not the credit card balance. They see the job title, but not the stress of needing every paycheck to maintain the lifestyle.

A person earning $300,000 annually can still be broke if their spending, debt, taxes, and obligations consume nearly everything they earn. High income creates more room for wealth building, but it also creates more room for expensive mistakes.

Many high earners fall into the same cycle:

They earn more, spend more, borrow more, and save less than they should.

At first, this cycle may not feel dangerous. Higher income can cover many errors for a while. A person can make payments, qualify for loans, upgrade their lifestyle, and still appear comfortable. But the underlying financial structure may be weak. If income drops, a business slows, a job disappears, health changes, or expenses rise, the fragility becomes obvious.

Income can hide financial weakness. Net worth reveals it.

The High-Income Trap

The high-income trap occurs when someone earns enough to look wealthy but not enough to become free because spending rises as fast as income.

This trap is common because lifestyle inflation feels natural. A raise becomes a better apartment. A promotion becomes a nicer car. A bonus becomes a vacation. A new business contract becomes a larger home. More income brings more options, and without a system, those options become expenses.

The danger is that each upgrade can become permanent. The larger home brings larger taxes, insurance, utilities, furnishing costs, and maintenance. The nicer car brings higher payments, insurance, registration, and repairs. Private schools, clubs, subscriptions, restaurants, travel, clothes, and entertainment can all become part of a lifestyle that requires constant high income to sustain.

Eventually, the person may feel trapped by the life their income created.

They may earn more than most people and still feel unable to slow down. They may want to change careers but cannot afford the pay cut. They may want to start a business but have too many obligations. They may want to invest more but have no monthly surplus. Their income is high, but their freedom is low.

This is why income alone is not the goal. The goal is to convert income into assets that increase net worth.

Net Worth Measures Real Progress

Net worth measures financial progress because it tracks ownership, savings, investments, debt reduction, and long-term growth.

Income tells you how much money flows into your life during a period of time. Net worth tells you whether that money is improving your financial position.

This difference matters deeply.

A person may receive a raise and feel richer. But if the raise is fully spent, net worth does not improve. A person may buy a luxury item and feel successful. But if the purchase adds debt or loses value quickly, net worth may decline. A person may live quietly, pay down loans, invest monthly, and increase cash reserves. Their lifestyle may not look dramatically different, but their net worth may be rising steadily.

Net worth is the scorecard that captures what income alone misses.

It reflects whether you are building assets. It reflects whether liabilities are shrinking. It reflects whether investments are growing. It reflects whether emergency savings are improving. It reflects whether business ownership, real estate equity, or retirement accounts are becoming stronger.

Net worth does not measure everything meaningful in life. It does not measure health, relationships, purpose, character, generosity, or happiness. But as a financial measurement, it is one of the clearest indicators of whether your money habits are building security or consuming it.

The Balance Sheet Is More Honest Than the Paycheck

A paycheck can be impressive. A balance sheet is honest.

The balance sheet shows what you own, what you owe, and what remains. It does not care about appearances. It does not care whether the car looks expensive, whether the clothes are designer, whether the vacation photographs impressed people, or whether the job title sounds powerful. It asks a simpler question: after all assets and liabilities are counted, what is your financial position?

This can be uncomfortable, especially for people who have used income as their main measure of success. But the discomfort is useful. A clear balance sheet can reveal problems early enough to fix them.

If debt is growing faster than assets, the balance sheet shows it. If investments are increasing, the balance sheet shows it. If lifestyle inflation is preventing wealth accumulation, the balance sheet shows it. If financial decisions are improving, the balance sheet shows that too.

Wealth builders learn to respect the balance sheet because it tells the truth before life forces the truth to become painful.

Assets Build Net Worth

Assets are the foundation of net worth growth.

An asset is something you own that has financial value. Some assets produce income. Some appreciate over time. Some provide liquidity. Some increase earning power. Some do several of these things at once.

Common wealth-building assets include savings, investment accounts, index funds, exchange-traded funds, dividend stocks, retirement accounts, real estate equity, rental property, businesses, intellectual property, and valuable skills that increase income.

Not all assets are equal. A savings account provides safety and liquidity but may not grow rapidly. Stocks can grow over time but fluctuate in value. Real estate may provide appreciation and cash flow but requires management, maintenance, and careful financing. A business can build significant wealth but carries risk and demands skill. Education and skills can increase income, but only when connected to real market value.

The goal is not to own random things. The goal is to own assets that strengthen your financial position.

When income is converted into assets, your financial life begins to change. Money no longer exists only to be spent. It becomes capital. Capital becomes ownership. Ownership can produce more income, appreciation, or options.

This is the central movement of wealth building: labor becomes capital, and capital becomes assets.

Liabilities Reduce Net Worth

Liabilities reduce net worth because they represent what you owe.

Some liabilities are part of normal financial life. A mortgage may help someone buy a home. A student loan may help someone access a higher-paying profession. A business loan may help fund productive expansion. Debt is not automatically bad.

But liabilities become dangerous when they fund consumption, depreciating purchases, or lifestyles that do not produce future value.

Credit card debt, payday loans, high-interest personal loans, expensive car loans, and financed luxury purchases can weaken net worth quickly. They create obligations that must be paid from future income. They also create interest costs that make the original purchase more expensive over time.

A liability is not only a number on a statement. It is a claim on future cash flow. Every debt payment reduces the amount of money available for saving, investing, or building flexibility.

This is why debt reduction can increase net worth even if your lifestyle does not visibly change. Paying down a loan improves the balance sheet. Reducing credit card balances strengthens your position. Eliminating high-interest debt frees future income.

Sometimes the most powerful wealth-building move is not buying a new asset. It is removing a liability that has been draining your progress.

Why Net Worth Changes Financial Behavior

Tracking net worth changes behavior because it makes financial consequences visible.

When people only track income, they may feel successful as long as money keeps coming in. When they track net worth, they begin to see whether the money is actually building anything.

A person who tracks net worth may think differently before taking on a car loan. They may ask how the debt will affect their balance sheet. They may think differently before carrying a credit card balance. They may ask whether the purchase is worth reducing future flexibility. They may think differently before spending a bonus. They may ask whether part of it should become savings, investments, or debt reduction.

Net worth tracking turns money management into a feedback system.

If net worth rises over time, your habits are likely moving in the right direction. If net worth stays flat despite good income, something is leaking. If net worth falls, the pattern needs attention.

Awareness improves decisions. Decisions improve outcomes.

Wealthy People Focus on Ownership

Real wealth comes from ownership.

Ownership may mean equity in businesses, shares of companies, real estate, intellectual property, cash-flowing investments, or other assets that can produce value. Wealthy people may still earn income, but they often focus on acquiring things that can grow, produce cash flow, or compound over time.

This is the difference between working only for money and owning assets that work alongside you.

A salary depends on continued labor. A business can produce profits beyond the owner’s direct hours if it is built well. A stock portfolio can grow through corporate earnings and market appreciation. A rental property can produce income if the numbers work. Intellectual property can earn revenue after the initial creation. Retirement accounts can compound over decades.

Ownership creates freedom because it reduces total dependence on wages.

This does not mean income is unimportant. Income often funds the first assets. But the purpose of income should not be endless consumption. The purpose of income is to support life while creating surplus that can be turned into ownership.

Income is the engine. Ownership is the destination.

Status Is Not Wealth

Status and wealth are often confused.

Status is what people can see. Wealth is what remains when nobody is watching.

Status may be displayed through cars, clothes, homes, restaurants, vacations, jewelry, devices, and social media. Wealth may be hidden in retirement accounts, brokerage accounts, business equity, paid-off debt, emergency funds, and appreciating assets.

The problem with status spending is that it can imitate wealth while destroying the ability to build it.

A person may spend heavily to appear successful, but those purchases may create no lasting value. They may even create debt. The appearance of wealth becomes a substitute for the reality of wealth.

This is one of the quiet tragedies of personal finance. People can work extremely hard, earn respectable incomes, and still struggle because too much money is spent defending an image.

The goal is not to look rich. The goal is to become financially secure.

How to Calculate Your Net Worth

Calculating net worth is simple, but it requires honesty.

First, list your assets. Include cash, checking accounts, savings accounts, investment accounts, retirement accounts, home equity, real estate, business ownership, vehicles if you choose to count their realistic resale value, and other valuable assets.

Second, list your liabilities. Include credit card balances, student loans, car loans, personal loans, mortgages, business debt, medical debt, unpaid taxes, and any other money you owe.

Third, subtract liabilities from assets.

The result is your net worth.

For example, imagine a person with $20,000 in savings, $80,000 in investments, $180,000 in home equity, and $20,000 in other assets. Their total assets are $300,000. If they owe $70,000 on student loans, $20,000 on a car loan, and $10,000 on credit cards, their total liabilities are $100,000. Their net worth is $200,000.

The number does not need to be perfect to be useful. Some values, such as business ownership or real estate, may require estimates. The goal is not false precision. The goal is a clear, consistent measurement over time.

What Should Count as an Asset?

Not every valuable item needs to be included in your net worth calculation.

Some people include cars, jewelry, furniture, electronics, and collectibles. Others prefer a more conservative calculation that focuses on liquid assets, investments, real estate equity, and business ownership. Both approaches can work if used consistently, but conservative tracking often gives a clearer picture of financial strength.

A car may have resale value, but it usually depreciates and costs money to maintain. Furniture and electronics may have value, but selling them often produces far less than the original purchase price. Collectibles can be difficult to value and may not be easy to sell quickly.

For wealth-building purposes, it is useful to distinguish between lifestyle possessions and productive assets.

A productive asset has a stronger connection to future financial growth. It may produce income, appreciate, or support earning power. Lifestyle possessions may improve comfort or enjoyment, but they should not be mistaken for the foundation of wealth.

What If Your Net Worth Is Negative?

A negative net worth means liabilities exceed assets.

This can happen because of student loans, credit card debt, medical bills, business losses, car loans, or a period of low income. It can feel discouraging, but it is not a permanent identity. It is a financial starting point.

The goal is to improve the number over time.

If your net worth is negative, the first priority is often stabilization. Build a small emergency fund, avoid adding new high-interest debt, increase income where possible, and create a repayment plan. As debt decreases and savings rise, net worth begins to improve.

Progress may be slow at first, but every dollar of debt reduced and every dollar saved moves the number in the right direction.

A person with a negative net worth who is improving every month may be in a better long-term position than a high earner with a positive net worth who is moving backward.

Direction matters.

How to Increase Your Net Worth

Increasing net worth depends on two broad actions: increase assets and reduce liabilities.

That sounds simple, but it can be applied in many practical ways.

You can increase income and save more of the difference. You can reduce unnecessary expenses and redirect money toward investments. You can pay down high-interest debt. You can invest consistently in diversified assets. You can buy appreciating assets carefully. You can build business equity. You can avoid lifestyle inflation. You can improve skills that increase earning power.

Every financial decision affects net worth in some way.

A raise can increase net worth if part of it is saved or invested. A raise can do nothing for net worth if it is entirely spent. A debt payment can increase net worth by reducing liabilities. An investment contribution can increase assets. A bad loan can increase liabilities. A luxury purchase financed with debt can reduce future flexibility.

The wealth builder asks, “Will this decision improve my balance sheet?”

Increase Income, But Capture the Increase

Increasing income is powerful because it creates more room for saving, investing, and debt reduction. But income growth only improves net worth if part of the increase is captured.

This is where many people fail. They work hard to earn more, then allow every increase to disappear into lifestyle upgrades. Their effort rises, their stress rises, their spending rises, but their net worth barely moves.

A better approach is to assign new income before it gets absorbed.

When income increases, decide in advance where the increase will go. Some can improve lifestyle, but a meaningful portion should strengthen the balance sheet. That may mean increasing investment contributions, paying down debt faster, growing an emergency fund, or saving for an asset purchase.

The earlier this habit is built, the more powerful it becomes.

Reduce Debt Strategically

Debt reduction increases net worth because it lowers liabilities.

High-interest debt should usually be a priority because it creates the greatest drag on progress. Credit card balances, payday loans, and expensive personal loans can make it difficult to build wealth because interest consumes money that could have gone toward assets.

There are two common debt repayment methods. The debt avalanche method prioritizes the highest-interest debts first, which can save the most money mathematically. The debt snowball method prioritizes the smallest balances first, which can create motivation through quick wins.

The right method is the one you can follow consistently while avoiding new debt.

Debt freedom is not only about numbers. It changes the emotional experience of money. Fewer payments mean more flexibility. More flexibility means better choices. Better choices often lead to stronger net worth.

Invest Consistently

Investing is one of the main ways net worth grows over time.

Savings are important for stability and emergencies, but long-term wealth usually requires assets that can grow. Investments allow money to participate in business growth, interest, dividends, appreciation, and compounding.

Consistency matters more than perfection. Many people delay investing because they are waiting for the perfect time, the perfect amount, or the perfect strategy. Meanwhile, time passes.

Starting with a manageable amount and increasing contributions over time can be more effective than waiting for ideal conditions. The habit is part of the asset. A person who learns to invest regularly builds both financial capital and emotional discipline.

Markets will fluctuate. That is normal. Long-term investing requires patience, diversification, and the ability to stay focused when short-term conditions are uncomfortable.

Buy Appreciating and Income-Producing Assets

Net worth grows faster when you own assets that can appreciate, produce income, or both.

Appreciating assets rise in value over time, though not in a straight line and not without risk. Income-producing assets generate cash flow. Some assets, such as certain businesses or rental properties, may do both if managed well.

The key is to evaluate assets carefully. Not every stock is a good investment. Not every property produces profit. Not every business creates value. Not every course improves earning power. Wealth building requires judgment.

Strong assets are usually connected to real value. They represent ownership, cash flow, productivity, scarcity, usefulness, or earning power. Weak assets often depend only on hype, speculation, or the hope that someone else will pay more later.

The goal is not to chase every opportunity. The goal is to acquire assets that fit your knowledge, risk tolerance, timeline, and financial plan.

Avoid Lifestyle Inflation

Lifestyle inflation is one of the biggest enemies of net worth.

It occurs when spending rises automatically with income. The person earns more but does not become wealthier because every raise creates new expenses.

A controlled lifestyle does not mean a joyless life. It means choosing upgrades carefully and allowing income growth to improve the balance sheet before it expands consumption.

One practical rule is to increase savings and investments whenever income rises. Another is to delay major lifestyle upgrades until net worth milestones are reached. This connects spending to financial strength rather than impulse.

Lifestyle inflation is dangerous because it feels like success. But if it prevents asset accumulation, it can quietly delay freedom for decades.

Track Your Net Worth Regularly

Tracking net worth monthly or quarterly creates awareness.

The process does not need to be complicated. A simple spreadsheet can work. List assets, list liabilities, calculate the difference, and compare it over time. The goal is not to obsess over every fluctuation. The goal is to notice the trend.

Some assets, such as investments, will move up and down with markets. Real estate values may change slowly and may be estimated. Business values may be difficult to measure. Debt balances should be easier to track. Cash and investment accounts can be updated regularly.

The most important question is whether your financial position is improving over time.

Tracking creates accountability. It also provides encouragement. Debt repayment may feel slow until you see liabilities falling month after month. Investing may feel small until you see assets rising over years. Emergency savings may feel boring until you recognize how much stability it creates.

Wealth often grows quietly. Tracking helps you see it.

Signs Your Net Worth Is Growing

There are several signs that your net worth is moving in the right direction.

Debt is decreasing. Investments are increasing. Emergency savings are growing. Assets are producing income. Your monthly obligations are becoming easier to manage. You feel less financial stress. You have more options. You are less dependent on every paycheck. You can handle unexpected expenses without panic. You are making decisions from a stronger position.

These signs may not look dramatic from the outside. That is part of the point.

Real wealth often grows quietly before it becomes obvious. The early signs are not always luxury purchases or public success. They are lower debt balances, larger investment accounts, more cash reserves, stronger skills, better decisions, and reduced fear.

Financial confidence comes from structure, not performance.

Net Worth and Financial Freedom

Financial freedom does not come from income alone. It comes from having enough assets, low enough liabilities, and enough flexibility to make choices without being controlled by financial pressure.

A high income can support freedom if it is used well. But if high income is tied to high spending and high debt, freedom remains distant. A person may be earning a lot while still being unable to pause, change direction, or absorb disruption.

Net worth is connected to freedom because it represents accumulated financial strength.

An emergency fund creates freedom from immediate panic. Investments create freedom through long-term growth. Debt reduction creates freedom from fixed obligations. Business ownership can create freedom through equity and income. Real estate equity can create options. Skills create freedom by increasing earning power.

Freedom is built when these pieces work together.

Why Monthly Cash Flow Still Matters

Net worth matters more than income as a measure of wealth, but income and cash flow still matter.

A person can have a high net worth and still experience cash flow problems if too much wealth is tied up in illiquid assets. For example, someone may own property with equity but not have enough cash for emergencies. Another person may have business value on paper but irregular income.

This is why financial health requires both a strong balance sheet and healthy cash flow.

Income pays current bills. Cash reserves provide liquidity. Assets build long-term wealth. Low liabilities protect flexibility. These elements support one another.

The point is not to ignore income. The point is to stop mistaking income for wealth.

The Emotional Shift From Earning to Building

When people focus only on income, money can feel like something that constantly needs to be chased. The solution to every problem becomes earning more. More income, more work, more pressure, more performance.

When people focus on net worth, the mindset changes. Money becomes something to direct, preserve, and multiply. The question shifts from “How much did I make?” to “How much did I keep, invest, and convert into ownership?”

This shift reduces the pressure to perform wealth for other people.

A person focused on net worth may choose a modest car because the difference can be invested. They may live in a smaller home because flexibility matters more than appearances. They may avoid unnecessary debt because peace is worth more than status. They may invest quietly while others spend loudly.

This is not about being cheap. It is about being clear.

Common Net Worth Mistakes

One common mistake is counting income as wealth. A large paycheck can create confidence, but it is not wealth until some of it is retained and converted into assets.

Another mistake is ignoring debt because the monthly payment feels manageable. Payments can hide the true cost of a liability. The balance sheet shows the full obligation.

A third mistake is overvaluing lifestyle possessions. Items bought for consumption often lose value quickly and may not contribute meaningfully to financial security.

A fourth mistake is failing to track progress. Without measurement, people often underestimate debt, overestimate assets, and miss patterns in their financial behavior.

A fifth mistake is comparing lifestyles instead of balance sheets. The person who looks wealthy may be financially stressed. The person who looks ordinary may be quietly building freedom.

Comparison becomes less useful when you understand how invisible wealth can be.

A Practical Monthly Net Worth Routine

A monthly net worth routine can be simple.

Choose one day each month. Record cash balances, investment balances, retirement accounts, estimated real estate equity, business value if applicable, and other meaningful assets. Then record all debts: credit cards, loans, mortgages, and other obligations. Subtract liabilities from assets.

After calculating the number, write a brief note explaining what changed. Did investments rise because of contributions or market movement? Did debt fall because of extra payments? Did cash increase because spending was controlled? Did liabilities rise because of new borrowing? Did net worth fall because of a planned purchase, market decline, or overspending?

This note matters because it connects numbers to behavior.

Over time, the routine becomes a financial mirror. It shows the effect of habits. It also helps you celebrate progress that may not be visible day to day.

What Net Worth Teaches About Discipline

Net worth teaches that wealth is cumulative.

Small decisions add up. A monthly investment contribution may seem modest, but repeated over years it can become significant. A debt payment may seem routine, but each payment reduces liabilities. Avoiding one unnecessary upgrade may not change life immediately, but repeated restraint creates capital.

Discipline is not always dramatic. It is often quiet repetition.

The person who builds wealth does not need every decision to be perfect. They need the overall pattern to be strong. More assets than liabilities. More investing than unnecessary consumption. More patience than impulse. More ownership than appearance.

Net worth reveals the pattern.

Final Thought: Income Creates Opportunity, Net Worth Creates Freedom

Income matters. It pays bills, creates options, and provides the raw material for wealth building. But income alone does not make a person wealthy.

Net worth tells the deeper story.

It shows what you own, what you owe, and whether your financial position is improving. It reveals whether income is being converted into assets or consumed by liabilities. It shows whether debt is shrinking, investments are growing, and ownership is expanding.

The goal is not to look rich. The goal is to become financially secure.

A high income can create opportunity. Net worth creates freedom.

Start tracking your net worth monthly. Watch how your financial mindset changes when the question is no longer only, “How much did I earn?” but also, “How much did I keep, build, and own?”